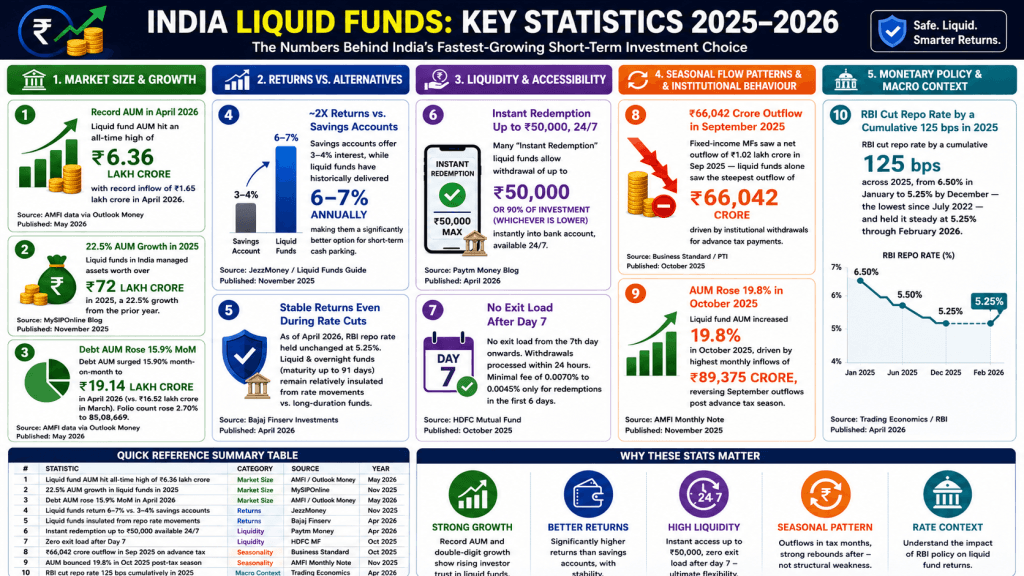

What are Liquid Funds | Risk, Returns & Benefits

The average Indian savings account earns around 2.5% to 3.5% interest per year. Inflation, meanwhile, runs at nearly twice that. This means every rupee sitting idle in your savings account is quietly losing purchasing power every single day. At the same time, investing in volatile options like equities is not suitable for short-term needs or emergency funds. This is where liquid funds come into the picture. They strike a balance between safety and accessibility, while also offering better returns than traditional savings options. They are designed for investors who want to park their money for short durations without taking significant risks.

This article breaks down everything you need to know about liquid funds, including how they work, the kind of returns you can expect, the risks involved, the benefits they offer, and whether they fit your financial plan or not.

What are Liquid Funds?

Liquid funds are a type of mutual fund that invests in very short-term financial instruments. These instruments typically have a maturity period of up to 91 days, which helps keep the risk relatively low.

In simple terms, when you invest in liquid funds, your money gets deployed into short-term lending opportunities such as:

Treasury Bills issued by the government

Commercial Papers issued by companies

Certificates of Deposit issued by banks

Short-term government securities

Because these investments mature quickly, the fund manager can regularly reinvest the money, which helps maintain liquidity and stability. Unlike fixed deposits, where early withdrawal may involve penalties, liquid funds allow you to withdraw your investment quickly, often within one working day.

The typical investment horizon for liquid funds can range anywhere from 1 day to 3 months, making them perfect for parking short-term idle cash, particularly for investors wanting a better alternative to a savings account without stepping into high-risk investments.

How do Liquid Funds Work?

As defined by SEBI (Securities and Exchange Board of India), liquid funds must invest only in debt and money market instruments with a maturity of up to 91 days. The following steps outline how the process works from an investor’s perspective:

The fund collects capital from investors

It deploys the money into high-quality, short-term instruments maturing within 91 days

Interest is earned on these instruments

The principal and interest are received upon maturity

The proceeds are reinvested continuously

Benefits of Liquid Funds

Liquid funds offer several practical advantages, especially for short-term goal planning.

1. High Liquidity

You can withdraw your money almost any time without worrying about long redemption periods, or penalties and lock-ins. Compared to a fixed deposit, where breaking out early means losing a chunk of your interest earnings, liquid funds offer a far quicker and stress free withdrawal, often within one working day.

2. Better Returns than Savings Accounts

Savings accounts in India typically offer 2.5% to 3.5% interest per year. Liquid funds have historically delivered returns in the range of 5% to 7% annually, though this is not guaranteed and changes with market conditions. But even a 2% difference can add up to a meaningful amount over several months.

3. Low Minimum Investment Amount

Most liquid funds let you begin with ₹500 to ₹1,000. There’s no pressure to commit a large amount, making them ideal for first-time investors who want to dip their toes into the world of mutual funds without committing a large capital.

4. Total Flexibility on Time

You can invest for just 1 day or stay invested for 3 months, there’s no fixed timeline. This makes liquid funds perfect for:

Parking money while you decide your next investment move

Building an emergency fund that still earns returns

Setting aside money for a short-term goal like a vacation or gadget purchase

5. Transparent and Regulated

Liquid funds in India are regulated by SEBI (Securities and Exchange Board of India), the government body that oversees all mutual funds. Every fund publishes its NAV daily, so you always know exactly what your investment is worth. There are no hidden surprises.

Risks of Liquid Funds

No investment is completely risk-free, and that includes liquid funds. Although these risks are considered small and manageable, it is important to understand them clearly before investing.

1. Credit Risk

Liquid funds invest in instruments issued by companies and governments. If a company defaults (fails to repay), the fund’s value could drop. This is very rare, since most funds stick to top-rated (AAA-rated) securities, but it has happened in the past. Always check the credit quality of a fund before investing.

2. Interest Rate Risk

When interest rates in the economy rise, the value of existing bonds falls. Since liquid funds hold very short-term instruments (maturing within 91 days), this risk is minimal, but not completely zero.

3. No Capital Guarantee

Unlike a fixed deposit in a bank, your principal in a liquid fund is not guaranteed by the government. That said, because these funds invest in high-quality, short-term instruments, significant losses are extremely rare.

4. Returns Are Not Fixed

You won’t always earn the same return. The yield changes based on interest rate movements and market conditions. If you need a guaranteed return, a liquid fund may not be the right tool.

For most conservative investors, these risks are well within a comfortable range, especially when compared to the volatility of equity mutual funds or direct stock market investments.

Who Should Invest in Liquid Funds?

Liquid funds are not just for wealthy investors or financial experts. They work well for a wide range of everyday situations:

People building an emergency fund. Financial advisors recommend keeping 3 to 6 months of living expenses easily accessible. Liquid funds are one of the best places for parking this money.

Investors waiting to enter equity markets. If you have a lump sum but aren’t sure when to invest in stocks or equity mutual funds, park it in a liquid fund temporarily.

Small business owners managing short-term cash flow between receivables and payables.

First-time investors who want a low-risk introduction to mutual fund investments.

If you’re unsure whether liquid funds are the right fit for your specific financial situation, speaking with a mutual fund advisor can make a significant difference. A good advisor will look at your income, goals, and risk appetite before making a recommendation.

Taxation of Liquid Funds

Liquid funds are taxed as debt mutual funds. Since most investors use them for short durations, the gains are almost always treated as short-term.

For investments made on or after April 1, 2023: All gains, regardless of how long you hold them, are added to your total income and taxed at your applicable income tax slab rate. There is no long-term capital gains benefit, even if you stay invested for several years.

For investments made before April 1, 2023: If held for more than 24 months and redeemed after July 23, 2024, a flat 12.5% LTCG tax applies without indexation.

Dividends: If you opt for the dividend plan instead of the growth plan, dividends are taxed at your slab rate, with TDS of 10% applicable on dividends exceeding ₹5,000.

For example, if you invest ₹1,00,000 and earn ₹5,000 as returns, this ₹5,000 is added to your taxable income and taxed at your slab rate, whether that’s 10%, 20%, or 30%.

It is important to factor in taxation when comparing returns with other instruments. A mutual fund consultant can help you understand the net post-tax return based on your specific income bracket.

Liquid Funds vs Savings Account vs Fixed Deposits

The following comparison provides context on how liquid funds measure up against other similar alternatives:

Feature | Liquid Funds | Savings Account | Fixed Deposit |

Risk Level | Low | Very Low | Very Low |

Typical Annual Returns | Market-linked (6.5% – 7%) | 2.5% to 3.5% | Fixed rate (typically 6% – 7%) |

Liquidity | T+1 | Instant | Penalty on early exit |

Lock-In Period | None | None | Yes |

Taxation | As per slab rate | As per slab rate | As per slab rate |

Overnight funds occupy a distinct position in this landscape. While they do not match the instant liquidity of a savings account or the fixed certainty of an FD, they offer a combination of low risk, transparency, and flexible exit that few comparable instruments can replicate for very short holding periods.

Practical Tips Before Investing

Liquid funds are simple to use, but a little due diligence goes a long way. Here’s what to keep in mind before you invest:

Check the expense ratio: This is the small annual fee the fund charges to manage your money. Even a seemingly minor difference in expense ratios can eat into your returns over time. Lower is generally better.

Look at the credit quality of the portfolio: A good liquid fund invests predominantly in AAA-rated instruments. If a fund is chasing slightly higher returns by investing in lower-rated securities, that’s a red flag.

Don’t chase returns: If one fund is offering noticeably higher returns than its peers, it’s likely taking on more risk to do so. Consistency and safety matter far more than marginally better yields in this category.

Use them for the right purpose: Liquid funds work best for short-term needs, like parking a bonus, building an emergency fund, or holding money between investments. They are not designed to be a long-term wealth-building tool.

If you’re unsure which fund suits your situation, a mutual fund advisor can help you evaluate your options and avoid common pitfalls, especially if you’re investing for the first time.

Conclusion

Liquid funds offer a simple and effective way to manage short-term money that would otherwise be sitting idle, slowly losing its value to inflation. They provide a balance of safety, liquidity, and moderate returns, making them suitable for emergency funds and temporary parking of surplus cash.

While they are not entirely risk-free, the level of risk remains relatively low compared to most other mutual fund categories. For investors who want easy access to their money without compromising too much on returns, liquid funds are one of the most practical and beginner-friendly tools available today.

Idle money is a missed opportunity, and liquid funds fix that without asking you to take on extra risk or lock away your savings. As with any investment, the key is to align your choice with your financial goals and time horizon. Get that right, and it’s one of the simplest upgrades you can make to how you manage your money, and the best time to start is now.

Frequently Asked Questions (FAQs)

1. Is my money safe in a liquid fund?

Liquid funds are considered one of the safest categories of mutual funds. They invest in high-quality, short-term instruments. However, unlike bank deposits, they are not completely risk-free. They carry a small degree of credit and interest rate risk. Choosing funds with AAA-rated portfolios reduces this risk significantly.

2. How quickly can I get my money back from a liquid fund?

In most cases, your money reaches your bank account within 24 hours of placing a redemption request. Some funds even offer instant redemption of up to ₹50,000 (or 90% of your investment, whichever is lower) directly to your bank account.

3. Are liquid funds better than fixed deposits?

It depends on your goal. If you need guaranteed returns and don’t mind locking your money away, an FD works well. But if you want flexibility, easy access, and returns that are slightly higher, liquid funds are the stronger choice for short-term parking.

4. Can I lose money in a liquid fund?

While extremely rare, it is technically possible for the NAV of a liquid fund to fall, usually due to a credit default in the fund’s portfolio. This has happened in a small number of cases historically. Picking well-managed funds with strong credit ratings significantly reduces this possibility

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Mutual fund investments are subject to market risks. Tax regulations are subject to change. Readers are advised to consult a qualified financial professional before making any investment decisions.

Tags: Liquid funds

Read Important Disclosures

You Might Also Like

Do It Yourself. Do It Smarter.

Download DIY App available on App Store & Google Play

OR