Tax filing is often assumed to be elective and unnecessary for some. However, the Government of India has made it mandatory for all the people to pay tax who are eligible & come under the tax slab. Unfortunately, many people are not aware that ITR filing bears amazing benefits for taxpayers. Hence, they either don’t file it, or their procrastination lets them be the victim of facing a penalty! Well, to guide you better, in this blog we will be discussing the mentioned below topics:

- What penalties are charged for late filing of ITR?

- What is an Income Tax Return?

- Who is required to file ITR?

What is an income tax return & why is it important to file an ITR?

Income Tax Return, commonly known as an ITR, is a form that needs to be submitted to the Income Tax Department. ITR contains basic information like a person’s income and the taxes that need to pay on it during the year. ITR could be filed either online or manually. The source of income might be different, check out the various forms such as:

- Income from salary (salaried employees)

- Profits and gains from business and profession

- Income from properties

- Income from capital gains

- Income from other sources such as dividends, interest on deposits, royalty income, winning on lottery, etc.

Who is required to file ITR?

You are obligated to file an ITR if your annual income comes under the mentioned tax slab:

Income Tax Slabs under the existing and old tax regime

Old Tax Regime

|

Income Slab |

Tax Rate |

|

Up to Rs. 2,50,000 |

Nil |

|

Rs. 2,50,001 to Rs. 5,00,000 |

5% of (Total income minus Rs. 2,50,000) |

|

Rs. 5,00,001 to Rs. 10,00,000 |

Rs. 12,500 + 20% of (Total income minus Rs. 5,00,000) |

|

Above Rs. 10,00,000 |

Rs. 1,12,500 + 30% of (Total income minus Rs. 10,00,000) |

New Tax Regime (default regime, FY 2025-26 / AY 2026-27)

|

Income Slab |

Tax Rate |

|

Up to Rs. 4,00,000 |

Nil |

|

Rs. 4,00,001 to Rs. 8,00,000 |

5% |

|

Rs. 8,00,001 to Rs. 12,00,000 |

10% |

|

Rs. 12,00,001 to Rs. 16,00,000 |

15% |

|

Rs. 16,00,001 to Rs. 20,00,000 |

20% |

|

Rs. 20,00,001 to Rs. 24,00,000 |

25% |

|

Above Rs. 24,00,000 |

30% |

Note: Under the new regime, a Section 87A rebate combined with the Rs. 75,000 standard deduction for salaried taxpayers makes income up to Rs. 12 lakh effectively tax-free. The new regime is the default; taxpayers without business income can choose the old regime each year if it works out more favourably for them.

Apart from this, there are other instances too when you should file an ITR if your total income has exceeded the basic exemption limit during the financial year. However, in a scenario where your gross total income does not exceed the basic exemption limit then the following are the points you need to consider: a) If your amount exceeds Rs 2 lakh on yourself or any other person for travel to a foreign country then you are liable to file ITR b)

If you have deposited more than Rs 1 crore in one or more current accounts maintained with a bank then you are liable to file ITR c) If your electricity bill has exceeded Rs 1 lakh in a single bill or on a yearly basis during the financial year then again you are liable to file ITR.

Also Read: Benefits of Filing Income Tax Returns on Time

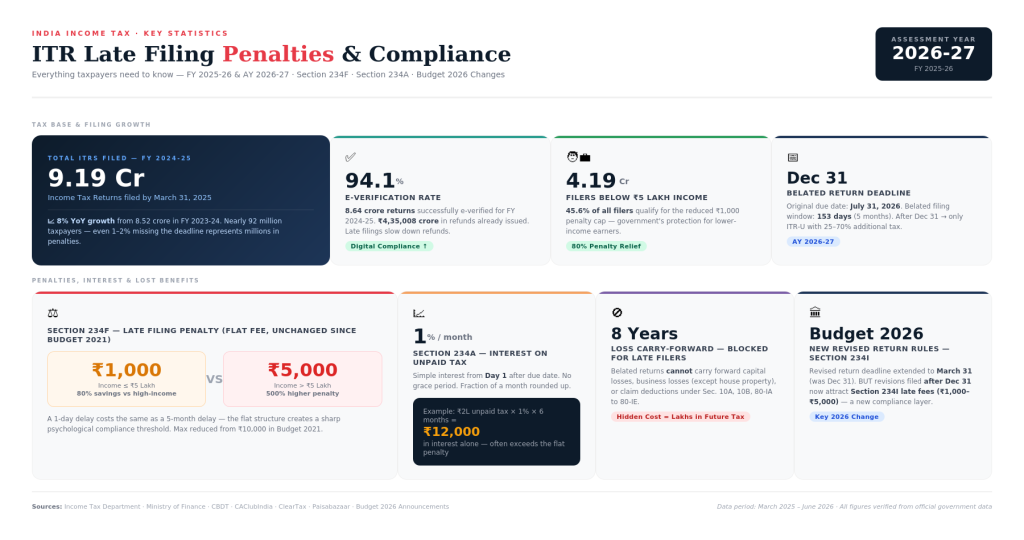

What is the penalty for ITR late filing?

If you are under the belief that by not filing an ITR you’ll be safe, then, unfortunately, this belief is wrong. Mentioned below are the charges that are associated with a delay in your ITF filings:

- Penalty Under Section 234F

Under section 234F of the Income Tax Act, filing your ITR after the due date makes you liable for a late fee. If your total income exceeds Rs 5 lakh, the penalty is Rs 5,000. If your total income is up to Rs 5 lakh, the penalty is capped at Rs 1,000. No late fee applies if your income is below the basic exemption limit, even if you file after the deadline.

For FY 2025-26 (Assessment Year 2026-27), the due date is 31st July 2026 for taxpayers filing ITR-1 or ITR-2, and 31st August 2026 for those filing ITR-3 or ITR-4 without a tax audit requirement. These dates follow the current notified schedule and have shifted in past years, so it is worth confirming on the e-filing portal closer to the deadline.

Note: The Income Tax Act, 1961 was replaced by the Income Tax Act, 2025, effective 1st April 2026. For ITR filings under AY 2026-27, the old section numbers, including 234F and 234A, still apply.

- Late Filing Fee Details

|

Total Income |

Penalty if filed after due date |

|

Up to Rs. 5,00,000 |

Rs. 1,000 |

|

Above Rs. 5,00,000 |

Rs. 5,000 |

|

Below basic exemption limit |

Nil |

Unlike the earlier rule structure, the penalty no longer depends on which part of the late-filing window you file in. The same flat fee applies any time after the due date, up to the belated return deadline of 31st December.

- Reduced Time for Revising Your Return

Mistakes happen when filings are rushed. Currently, you can revise your ITR without any additional fee until 31st December of the assessment year. Budget 2026 has proposed extending this window to 31st March of the following year, though a late fee would apply if the revision is filed after 31st December. Until this is formally notified, treat 31st December as the safe cutoff for fee-free revisions.

- Payment of Interest

As per section 234A, if you do not end up filing your tax returns on or before the due date then you will be liable to pay an interest of 1% every month or part thereof on the same amount. After the due date, the calculation of the penalty starts. Don’t wait too long to submit your ITR!

- Carry Forward of Losses is Not Permitted

If by any chance you have incurred a loss during the year in your business, then you have to make sure to file your return within the due date. If not then it will deprive you of carrying forward these losses for the next year. So, it is a necessary step to take, and make sure you take it.

This restriction applies to business losses and capital losses. Loss from house property is the one exception and can still be carried forward even if the return is filed late.

- Delay in Receiving Refunds

Not filing ITR results in delaying your receiving refunds from the government for the excess taxes you have ended up paying. If you wish to receive your refund without any delay then make sure you file your return before the due date.

- Missed the Belated Return Deadline Too?

If you miss even the belated return deadline of 31st December, you are not entirely out of options. You can still file an Updated Return (ITR-U), though it comes with additional tax and interest depending on how late you are. It is a costlier fallback, not a substitute for filing on time, but it is worth knowing it exists.