What is Micro SIP?

Micro SIP (Systematic Investment Plan) is a variant of the traditional mutual fund SIP tailored for very small, regular investments. Unlike a regular SIP (usually starting at ₹500 or more), micro SIPs let investors start with amounts as low as ₹100–₹250 per installment. This low entry point makes mutual funds accessible to students, daily wage earners, and first-time or low-income investors who cannot commit larger sums. Essentially, it’s the same disciplined investment strategy of investing fixed sums periodically, but at a “micro” level. For example, SBI Mutual Fund’s new JanNivesh plan allows SIP contributions of just ₹250 monthly, aligning with SEBI’s push for small-ticket investing. In short, a micro SIP is simply a SIP with a much lower minimum amount, helping broaden participation in the market

Why Micro SIP Matters

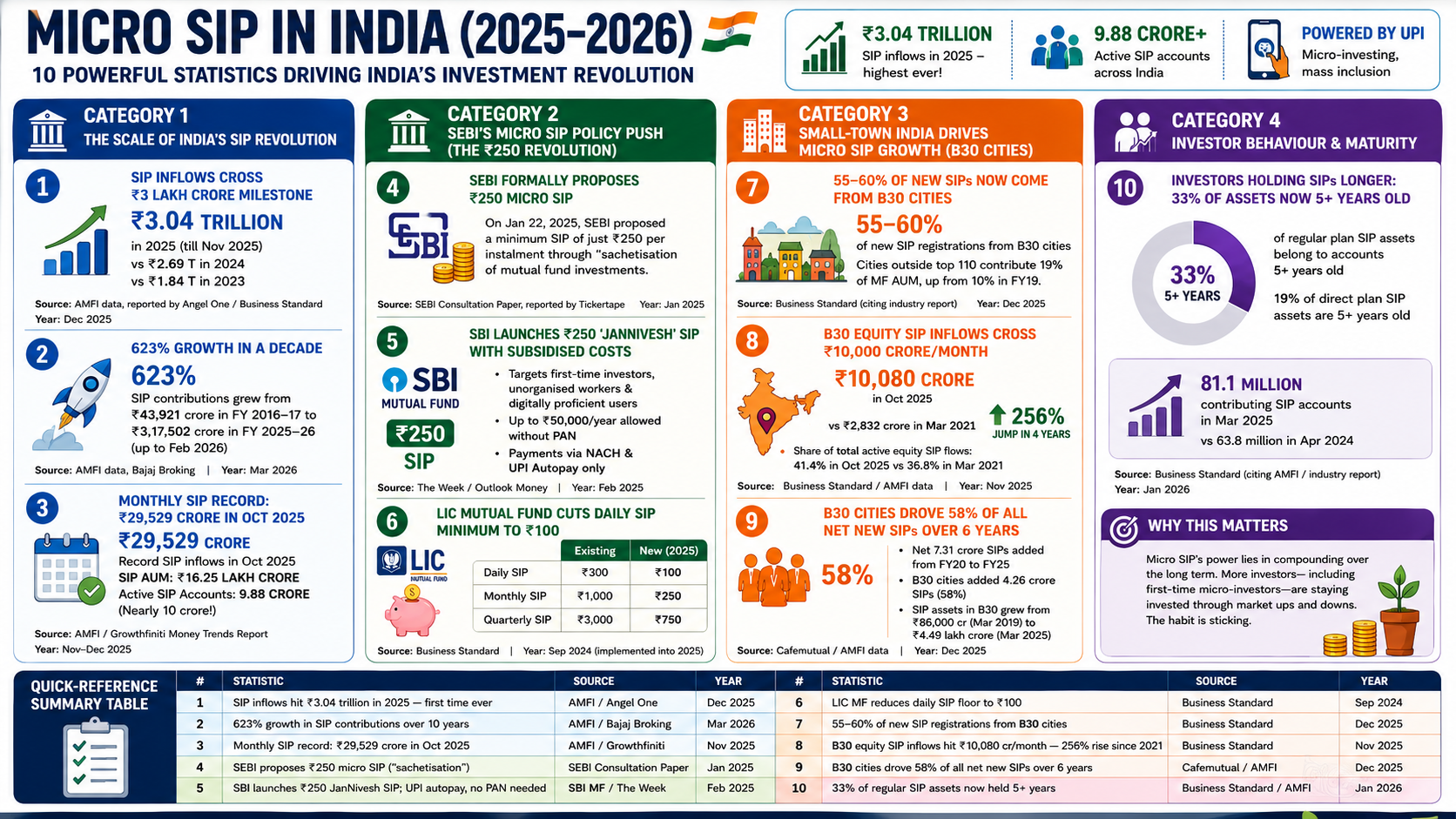

India’s mutual fund industry is booming, with Assets Under Management (AUM) reaching about ₹81.9 lakh crore by April 2026. Yet the investor base remains underpenetrated – fewer than 30 crore Indians invest in mutual funds despite India’s 140+ crore population. Micro SIPs directly address this gap by lowering the financial barrier. They promote financial inclusion by encouraging saving habits across urban and rural India. SEBI and industry leaders emphasize that even a small SIP (₹250) is “one of my fondest dreams” for growing the investor base[7]. By launching products like SBI’s JanNivesh (₹250 SIP) and pushing AMCs to offer ₹100 SIPs, regulators aim to bring more first-time investors on board. This means a shopkeeper, a farmer, or a student can start wealth-building in mutual funds with pocket money-sized investments.

Micro SIPs also lock in financial discipline for new investors. Regular small investments cultivate the habit of saving. Over time, even tiny monthly SIPs benefit from rupee cost averaging and compound returns. In essence, micro SIPs matter because they turn minimal savings into substantial long-term wealth while broadening participation in mutual funds.

How Micro SIP Works

A micro SIP functions like any SIP: you set up automatic periodic investments into a chosen mutual fund. The key difference is the amount and some regulatory features. First, you pick a mutual fund scheme that allows small SIPs (many funds now permit ₹100 or ₹250 SIPs). Then, you complete KYC (Know Your Customer) formalities – SEBI has eased requirements so PAN is not mandatory for micro SIPs up to ₹50,000 per year. In fact, SEBI’s new guidelines allow Aadhaar-based KYC and use of NACH/UPI for auto-debits. You link your bank for auto-pay (using NACH mandate or UPI AutoPay), choose your SIP date and frequency (monthly or fortnightly), and authorize the small amount (e.g. ₹100) each cycle.

Regulations for micro SIPs include committing to about 5 years (60 installments). However, withdrawals are generally allowed anytime (subject to market conditions), since SIPs are market-linked investments. SEBI also allows up to three separate micro SIPs of ₹250 in different fund houses. Importantly, micro SIPs usually run in growth plans only (no debt or small/mid-cap funds), to align with the inclusion goal. Once set up, each cycle debits the small sum and buys mutual fund units at that day’s NAV. Over months and years, these purchases build your portfolio. The process is simple and automated – you don’t need to time the market, and every small SIP goes into the fund even if markets fluctuate.

Step-by-Step: Starting a Micro SIP

- Define Your Goal: Decide why you’re investing – e.g. create an emergency fund, save for a child’s education, or build a retirement corpus. Having a goal (amount and horizon) helps in choosing the right strategy.

- Complete KYC: Use Aadhaar-based e-KYC if possible. For micro SIPs up to ₹50k/year, a basic KYC (without PAN) is permitted. Verify your identity and address to open an MF account.

- Select a Fund: Research mutual fund schemes that allow small SIPs. Look for stable track records, low expense ratios, and fit for your goal. Many equity or hybrid funds have launched micro SIP options. For example, SBI’s JanNivesh SIP invests in the SBI Balanced Advantage Fund.

- Choose a Platform: Register on a digital platform or go through an adviser that supports micro SIPs. Popular options include Groww, Zerodha Coin, Paytm Money, or AMC websites. These platforms often have built-in SIP planners and calculators.

- Set Amount and Frequency: Decide your micro SIP amount (₹100, ₹250, etc.). SEBI’s new rule supports Rs.250 monthly or fortnightly SIPs. Enter the amount, select date, and how often (monthly/fortnightly).

- Enable Auto-Pay: Link your bank account via NACH or UPI Autopay. This ensures the micro SIP installments are debited automatically each period.

- Stay Consistent: Even small ₹100 SIPs should run regularly. This consistency triggers rupee cost averaging and compounding. Check your statements periodically, but generally let the SIP continue unless goals change.

With these steps, your micro SIP will start accumulating units in your chosen fund each cycle. Over time, the power of compounding can turn even pocket-change investments into a meaningful corpus

Micro SIP vs Regular SIP: Comparison

| Features | Micro SIP | Regular SIP |

| Minimum Investment | ~₹100–₹250 per month | Typically ₹500 or more |

| Target Investors | New/small investors (students, wage earners) | All investors |

| SEBI Incentives | ₹500 incentive for distributor after 24 installments (for ₹250 SIP) | Not applicable |

| Allowed Funds | Growth plans only (no debt, mid/small-cap) | Any mutual fund schemes |

| Investment Commitment | Ideally ~5 years (60 installments) | Flexible (stop anytime) |

| KYC Requirements | Aadhaar-based KYC; PAN not mandatory up to ₹50k/year | Standard KYC (PAN, Aadhaar) required |

| Expense Impact | High cost ratio per amount (fund fees may be larger fraction of small SIP) | Lower relative impact of fees |

| Flexibility | Can pause/stop any time, but geared to long-term habit | Equally flexible; any tenure |

| Compound Effect | Builds corpus slowly; compounding over very long term | Similar compounding; faster corpus growth with larger SIPs |

This table shows micro SIPs lower the entry barrier significantly, but come with trade-offs in terms of scale and fund choice. Both use the same SIP mechanism of regular investing.

Top SIP Planner Tools & Advisors

A SIP planner (or SIP calculator) is a digital tool that helps map out your investments and goals. These online tools can project future corpus based on different SIP amounts, rates and durations. Top platforms in India include Groww, Zerodha’s Coin, Paytm Money, Kuvera, and ET Money – they all have free SIP calculators and tracking dashboards. For example, Groww offers an interactive SIP calculator to estimate returns, and Zerodha Coin has features for step-up SIP planning.

For expert guidance, consider financial advisory services. Registered Investment Advisors (RIAs) and robo-advisors like Fincart, Scripbox or smallcase provide goal-based SIP planning. They suggest which funds to pick and even automate SIP setups. Some mutual fund houses (like SBI, HDFC, Aditya Birla) also offer SIP advisory via their customer service. The key is that the best SIP planner is one that matches your needs – a tool that is user-friendly, accurate, and aligned with your goals. Automated planners encourage disciplined investing by setting up SIP schedules and reminders. Ultimately, a combination of reliable digital tools (for ease and tracking) and qualified advice (for strategy) works best.

Choosing the Best SIP Planner or Advisor

When selecting a SIP planner or advisor, focus on credibility and fit. Look for planners with a proven track record, experience and certification. Check if they have reputable credentials (like SEBI RIA registration or certifications) and transparent fee structures. Reviews and recommendations from peers can help assess reliability. Importantly, the planner should understand your goals and risk tolerance. A good SIP planner customizes recommendations (funds, amounts, timelines) to your situation rather than offering one-size-fits-all solutions.

Compare tools based on ease of use. A top SIP calculator should allow you to adjust investment amounts (even ₹100 vs ₹500), expected returns, and tenure easily. Mobile apps with reminders and auto-top-up features (step-up SIP) can boost success. Finally, if using a financial advisor, ensure they prioritize your financial well-being and charge reasonable advisory fees. In summary, the best SIP planner/advisor is one that is experienced, transparent, and aligns with your goals, whether it’s an app, a robo-advisor, or a human consultant.

Pros & Cons of Micro SIP

Pros:

- Low Barrier: Invest with just ₹100–₹250. Accessible to virtually everyone, even with tight budgets

- Financial Discipline: Automating tiny SIPs helps build saving habits and sticks to regular investing

- Inclusion & Flexibility: Opens mutual fund investing to new segments (students, homemakers, rural investors). Users can pause or stop SIP any time without penalties.

- Compounding: Even small amounts grow over long horizons thanks to compounding. For instance, a ₹250 monthly SIP at ~12-14% could become crores in a few decades. Note: Mutual fund returns are market-linked and not guaranteed. Historical equity fund return of 12–14% p.a. over the long term is indicative only; actual returns may vary.

Cons:

- Slow Wealth Accumulation: Small monthly contributions take much longer to build significant corpus compared to higher SIPs. It requires patience and long horizons (10-20+ years)

- Fund Selection Limits: SEBI’s micro-SIP rules restrict scheme choice (growth plans only). Also, some high-return equity funds have higher minimums, so micro investors may miss certain opportunities.

- Cost Sensitivity: Expense ratios and fees remain the same percentage-wise, so a ₹100 SIP may see a larger fraction eaten by fees than a larger SIP. Low SAC or direct plans can help mitigate this.

In short, micro SIPs offer inclusivity and discipline but must be viewed as a long-term strategy. They are ideal as a starting point, but investors should step up amounts or add higher-SIP funds over time to meet big goals.

Key Takeaways

- Micro SIP Basics: A Micro SIP lets you invest as little as ₹100–₹250 per month in mutual funds. It’s designed to onboard new, small investors with minimal entry barriers.

- Accessibility: With SEBI’s push, many AMCs (SBI, HDFC, Aditya Birla, etc.) now offer micro-SIP plans. Aadhaar-based KYC and UPI/NACH auto-debits make setting up a ₹100 SIP quick and simple.

- Discipline & Compounding: Even tiny SIPs grow meaningfully over decades. For example, ₹250/month at 12–15% could exceed ₹1 crore in 30–40 years, showcasing the power of disciplined micro-investing.

- Planning Tools: Use SIP calculators and goal planners (Groww, Zerodha Coin, etc.) to project returns and tailor your strategy. A good planner/advisor will consider your goals, risk profile, and suggest the right funds.

- Compare SIP Options: Micro SIPs vs regular SIPs – micro SIPs have lower minimums but longer horizons. Before choosing, compare fees, expected return, and any restrictions (e.g. micro SIPs may exclude some funds).

- Stay Flexible: You can pause or stop a SIP anytime. Micro SIPs require commitment to see benefits, but also allow flexibility. Gradually increase SIP amounts when you can (step-up SIP) to amplify wealth creation.

- Financial Advice: Consulting a certified SIP planner or using reputable fintech tools adds confidence. Look for advisors with proven credentials and personalized advice.

By following these principles, even the smallest monthly investment can become part of a powerful, long-term wealth-building strategy.

FAQ Section

Q: What is a Micro SIP and how does it differ from a regular SIP?

A: A Micro SIP (Systematic Investment Plan) is a type of mutual fund investment that allows extremely small periodic contributions, often starting at just ₹100–₹250. It differs from a regular SIP mainly in the minimum investment amount (micro SIPs have a much lower floor). Both use automatic periodic investing, but micro SIPs target first-time or low-income investors. SEBI has also introduced regulatory support (like Aadhaar KYC and distributor incentives) specifically for micro SIPs.

Q: How can I start a Micro SIP in India?

A: To start a Micro SIP, complete your KYC (PAN or Aadhaar) with a mutual fund provider or platform. Then choose a fund that offers small SIPs and decide your amount (e.g. ₹100). Link your bank using NACH or UPI autorisation and set the SIP date and frequency (monthly or fortnightly). Once activated, the amount will auto-debit each cycle. Platforms like Groww, Zerodha Coin, and SBI MF’s portal allow easy online sign-up. SEBI’s rules mean you don’t need PAN for annual investments up to ₹50,000.

Q: What are the benefits of a Micro SIP?

A: The main benefits are affordability and inclusion. You can start investing with very little money. Micro SIPs instill discipline (regular savings habit) and leverage rupee cost averaging and compound interest for wealth creation. They open mutual funds to students, homemakers, and others who can’t afford large sums.

Q: Are micro SIPs available for all mutual funds?

A: Not all funds. By SEBI regulation, micro SIPs (₹250 SIPs) are currently limited to growth plan schemes and exclude debt, sector/thematic, and small-/mid-cap funds. However, many AMCs voluntarily allow ₹100 SIPs on their equity or hybrid funds. For example, Zerodha FundHouse offers SIPs from ₹100 in most funds (aside from ELSS, which has a ₹500 minimum). So check each fund’s minimum SIP policy; many large-cap and balanced funds will support micro investments.

Q: How do I choose the best SIP planner or advisor?

A: Look for a planner with a strong track record and qualifications. Good questions include: Do they understand your goals? Are their fees transparent? Do they provide personalized advice? Online SIP planners should be user-friendly and allow goal-based calculations. Read reviews or get referrals. If using a human advisor, ensure they’re registered (e.g. SEBI RIA) and prioritize your interests.

Q: Can I stop or withdraw a Micro SIP anytime?

A: Yes. Like regular SIPs, micro SIPs are flexible investments. You can pause or stop the SIP anytime through your platform. You can also redeem the accumulated units at any time (subject to market conditions). There’s no lock-in on micro SIPs themselves (unlike some specific products). Just keep in mind that stopping early may reduce long-term returns.

Q: Who should consider a Micro SIP?

A: Micro SIPs are ideal for beginners and individuals with limited budgets. If you find it hard to save lumpsum amounts, or want to build wealth gradually, a micro SIP can get you started. It’s also a great way to instil saving discipline. Once you’re comfortable, you can increase the SIP amount or add more funds to accelerate growth.