“Risk comes from not knowing what you’re doing” – Warren Buffett

When it comes to building long-term wealth in India, one of the most fundamental decisions every investor faces is choosing between an equity vs debt mutual fund. Both are popular investment vehicles — but they serve very different purposes, carry different risks, and are suited to different financial goals and timelines.

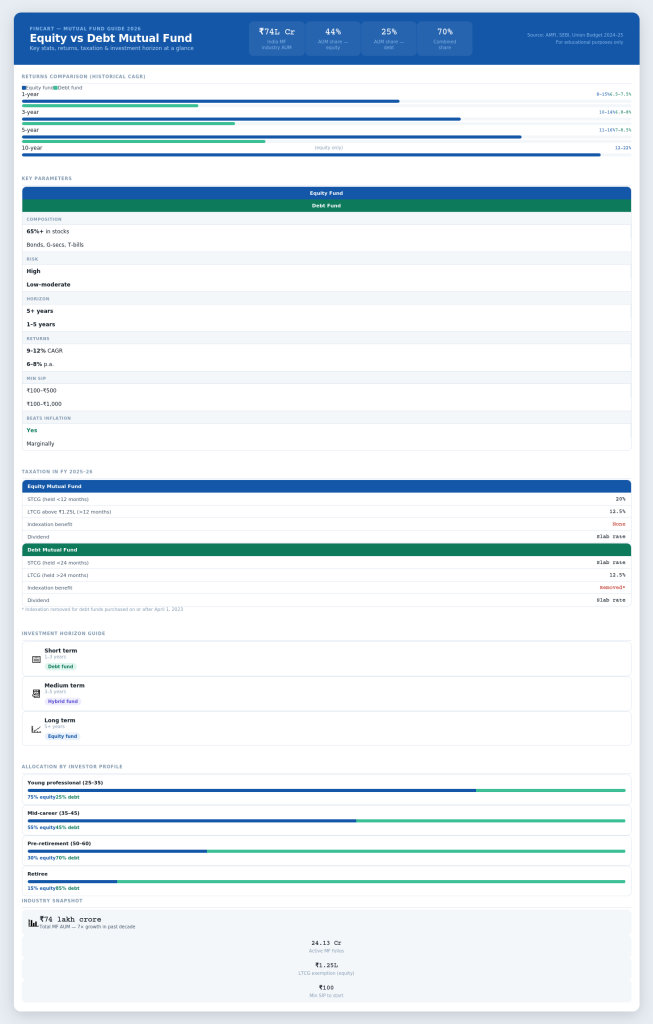

According to the Association of Mutual Funds in India (AMFI), the mutual fund industry’s total Assets Under Management (AUM) crossed ₹74 lakh crore in 2025. Equity and debt mutual funds together account for nearly 70% of this figure. Despite the massive growth, many investors remain confused about the core debt and equity mutual funds difference — and that confusion often leads to poor investment decisions.

In this guide, we break down everything you need to know about the equity vs debt mutual fund debate — including real return benchmarks, updated 2026 tax rules, a side-by-side comparison table, and a clear framework to help you decide which fund suits your financial goals. And if you’re still unsure, consulting a qualified mutual fund advisor or mutual fund consultant can help you build a portfolio tailored to your life.

What Is an Equity Mutual Fund?

An equity mutual fund primarily invests a minimum of 65% of its assets in equity shares of companies listed on stock exchanges. The goal is capital appreciation — growing your wealth over time by participating in the profits and growth of businesses.

Types of Equity Mutual Funds

- Large-Cap Funds — invest in the top 100 companies by market capitalisation; relatively more stable

- Mid-Cap Funds — invest in companies ranked 101–250; higher growth potential with moderate risk

- Small-Cap Funds — invest in companies ranked 251 and beyond; highest growth potential but also highest volatility

- Flexi-Cap / Multi-Cap Funds — invest across all market capitalisations, offering dynamic diversification

- ELSS (Tax-Saving Funds) — equity funds with a 3-year lock-in that qualify for tax deductions under Section 80C

Key Characteristics

- Returns: Historically 9%–12% CAGR over long periods (5+ years)

- Risk: High — returns are tied to stock market performance

- Best for: Long-term wealth creation, retirement planning, beating inflation

- Recommended investment horizon: 5 years and above

Equity mutual funds are also called growth funds and are ideal for investors who are willing to tolerate short-term volatility in exchange for significantly higher long-term returns.

What Is a Debt Mutual Fund?

A debt mutual fund invests in fixed-income instruments such as government securities, treasury bills, corporate bonds, and commercial paper. The goal is income generation and capital preservation, not aggressive growth.

Types of Debt Mutual Funds

- Liquid Funds — invest in instruments with maturity up to 91 days; highly liquid, low risk

- Short-Duration Funds — hold instruments with 1–3 year maturity

- Gilt Funds — invest exclusively in government securities; virtually no credit risk

- Fixed Maturity Plans (FMPs) — close-ended funds with a fixed investment horizon

- Corporate Bond Funds — invest in high-rated corporate bonds for slightly higher yields

- Dynamic Bond Funds — actively managed to benefit from interest rate movements

Key Characteristics

- Returns: Typically 6%–8% annually, depending on the fund category and interest rate environment

- Risk: Low to moderate — subject to interest rate risk and credit risk, not equity market risk

- Best for: Short to medium-term goals, capital preservation, regular income needs

- Recommended investment horizon: 1–3 years (short-term), 3–5 years (medium-term)

Understanding the debt and equity mutual funds difference begins here — one chases growth through market participation, the other seeks stability through fixed-income instruments.

Equity vs Debt Mutual Fund: Side-by-Side Comparison

The table below gives you a comprehensive look at the equity vs debt mutual fund comparison across all critical parameters:

| Parameter | Equity Mutual Fund | Debt Mutual Fund |

| Primary Investment | Company stocks / equity shares | Bonds, government securities, treasury bills |

| Return Potential | High (9%–12% CAGR, long-term) | Moderate (6%–8% annually) |

| Risk Level | High (market-linked) | Low to Moderate |

| Volatility | High in short term | Low |

| Investment Horizon | 5+ years | 1–3 years (short), 3–5 years (medium) |

| STCG Tax | 20% (held < 12 months) | Added to income, taxed at slab rate |

| LTCG Tax | 12.5% above ₹1.25 lakh (held > 12 months) | 12.5% (held > 24 months, no indexation) |

| Best for | Long-term wealth creation, retirement | Capital preservation, short-term goals |

| Inflation Beating | Yes (typically outpaces inflation) | Marginally (may not always beat inflation) |

| Liquidity | High (open-ended funds) | High (especially liquid funds) |

| Minimum SIP Amount | ₹100–₹500 | ₹100–₹1,000 |

| SEBI Regulation | Min. 65% in equities | Primarily in debt instruments |

This debt and equity mutual funds difference table should serve as your quick reference whenever you are evaluating the two fund categories.

Return Comparison: How Much Have They Actually Delivered?

One of the most important factors in the equity vs debt mutual fund debate is actual historical performance.

Equity Mutual Fund Returns (Historical CAGR)

| Time Period | Average Equity Fund Return (Approx.) |

| 1 Year | 8%–15% (varies widely with market) |

| 3 Years | 10%–14% |

| 5 Years | 11%–16% |

| 10 Years | 12%–18% (large-cap), 15%–22% (mid/small-cap) |

Note: Past performance is not a guarantee of future results. The above figures represent average performance across diversified equity funds in India.

Debt Mutual Fund Returns (Historical)

| Fund Category | Typical Annual Return |

| Liquid Funds | 6.5%–7.5% |

| Short Duration Funds | 6.8%–8% |

| Corporate Bond Funds | 7%–8.5% |

| Gilt Funds | 6.5%–9% (depends on rate cycle) |

| Dynamic Bond Funds | 7%–9% |

The verdict: Equity mutual funds deliver significantly higher returns over long periods. However, this comes with the trade-off of short-term volatility — in any given year, equity funds can generate negative returns. Debt funds offer relatively predictable, stable returns with far less fluctuation.

Taxation on Equity vs Debt Mutual Fund in 2026

Taxation is one of the most critical — and most commonly ignored — factors in the equity vs debt mutual fund decision. Here is the updated tax structure for FY 2025–26:

Equity Mutual Fund Taxation

- Short-Term Capital Gains (STCG): If you redeem units held for less than 12 months, gains are taxed at 20% (revised from 15% in the Union Budget 2024)

- Long-Term Capital Gains (LTCG): If you hold for 12 months or more, gains above ₹1.25 lakh per financial year are taxed at 12.5% without indexation benefit

- Dividend Income: Taxed at the investor’s applicable income tax slab rate

Debt Mutual Fund Taxation

- Short-Term Capital Gains (STCG): If held for less than 24 months, gains are added to your total income and taxed at your income tax slab rate

- Long-Term Capital Gains (LTCG): If held for 24 months or more, gains are taxed at 12.5% without indexation benefit (indexation benefit was removed in Budget 2023 for debt funds purchased on or after April 1, 2023)

- Dividend Income: Taxed at your applicable slab rate

Key Tax Insight: The removal of the indexation benefit for debt funds has made them relatively less tax-efficient than they once were for long-term investors, narrowing the tax advantage they previously held over fixed deposits.

A qualified mutual fund advisor or mutual fund consultant can help you structure your investments in a tax-efficient manner, especially if you are in a higher income tax bracket.

Investment Horizon Guide: Which Fund for Which Goal?

Choosing the right fund type begins with knowing your time horizon and financial goal. Here is a clear framework for the equity vs debt mutual fund decision:

Short-Term Goals (1–3 Years)

Recommended: Debt Mutual Funds

If you are saving for a vacation, a car purchase, a wedding, or building an emergency fund, debt funds — especially liquid funds or short-duration funds — are the appropriate choice. They offer capital safety, reasonable returns of 6.5%–8%, and high liquidity. Equity funds are too volatile for such short timelines.

Medium-Term Goals (3–5 Years)

Recommended: Hybrid Funds or a Mix of Equity + Debt

For goals like a down payment on a house or saving for higher education, a combination of equity and debt (or hybrid/balanced advantage funds) works well. This gives you growth potential while managing downside risk.

Long-Term Goals (5+ Years)

Recommended: Equity Mutual Funds

For goals like retirement planning, children’s education fund (10+ years away), or building long-term wealth, equity mutual funds are the most appropriate choice. The longer the investment horizon, the lower the effective risk of equity funds — because market volatility smooths out over time, and the compounding effect works powerfully in your favour.

Risk Comparison: Understanding What You Are Taking On

Risk is perhaps the most misunderstood element in the equity vs debt mutual fund comparison.

Equity fund risks include:

- Market risk: Stock prices fluctuate based on economic conditions, corporate earnings, global cues, and investor sentiment

- Concentration risk: Sector-specific or thematic funds can be highly concentrated

- Liquidity risk: Small-cap stocks may be harder to sell in falling markets

Debt fund risks include:

- Interest rate risk: When interest rates rise, bond prices fall — impacting returns

- Credit risk: If the company that issued a bond defaults, the fund’s NAV can drop sharply

- Liquidity risk: Some long-duration or low-rated paper may be hard to exit quickly

Understanding these risks is precisely why working with a mutual fund advisor is valuable. A good mutual fund consultant will not only match funds to your goals but will also stress-test your portfolio against different risk scenarios.

Who Should Invest in What? Investor Profiles Explained

| Investor Profile | Recommended Fund Type |

| Young professional (age 25–35), long horizon | 70–80% equity, 20–30% debt |

| Mid-career investor (age 35–45), balanced goals | 50–60% equity, 40–50% debt |

| Pre-retirement (age 50–60), capital protection focus | 30% equity, 70% debt |

| Retiree, regular income needed | 10–20% equity, 80–90% debt/hybrid |

| Short-term goal (1–2 years) | 100% debt |

| High-risk appetite, long horizon | 80–100% equity |

No single answer fits every investor — the right equity vs debt mutual fund allocation depends entirely on your age, income, financial goals, risk tolerance, and investment horizon.

The Middle Ground: Hybrid Mutual Funds

If the equity vs debt mutual fund choice feels overwhelming, hybrid mutual funds offer a ready-made middle path. These funds invest in both equity and debt instruments in varying proportions, making them suitable for investors who want growth with some cushion against volatility.

Types of Hybrid Funds

- Aggressive Hybrid Funds: 65%–80% equity, 20%–35% debt — best for moderate risk takers with a 3–5 year horizon

- Conservative Hybrid Funds: 10%–25% equity, 75%–90% debt — ideal for conservative investors

- Balanced Advantage Funds (BAFs): Dynamically adjust equity-debt allocation based on market valuations — suited to goal-based investing

- Multi-Asset Funds: Invest across equity, debt, and commodities (including gold)

Hybrid funds are an excellent starting point for first-time investors who are still learning the debt and equity mutual funds difference and are not yet comfortable making allocation decisions on their own.

How a Mutual Fund Advisor or Mutual Fund Consultant Can Help

The equity vs debt mutual fund decision is not a one-time choice — it is an ongoing portfolio management exercise that evolves as your life circumstances change. This is where professional guidance becomes invaluable.

A mutual fund advisor can help you:

- Assess your risk profile through a structured questionnaire and financial health review

- Map your financial goals (retirement, children’s education, home purchase) to the right fund types

- Build a diversified portfolio that balances equity vs debt allocation correctly

- Review and rebalance your portfolio as markets move and your goals shift

- Navigate the tax implications of redemptions and switches between funds

- Avoid common investor mistakes like chasing past returns or panic-selling during corrections

A mutual fund consultant at Fincart works with you across your entire financial journey — not just in selecting funds, but in integrating mutual fund investments with your tax planning, insurance, and retirement strategy. Our certified wealth managers have collectively managed the portfolios of hundreds of families across India, and they bring experience, empathy, and expertise to every client relationship.

If you are uncertain about the right equity vs debt mutual fund mix for your goals, consult a Fincart mutual fund advisor today — and get a free portfolio review.

Equity vs Debt Mutual Fund: Quick Decision Checklist

Ask yourself these questions to narrow down your choice:

- What is my investment goal? (Wealth creation → equity; Capital preservation → debt)

- How long can I stay invested? (5+ years → equity; 1–3 years → debt)

- How much volatility can I handle? (High → equity; Low → debt)

- What is my tax bracket? (Higher bracket investors may benefit from certain debt structures)

- Do I need regular income? (Yes → debt/hybrid; No → equity)

- Am I a first-time investor? (Consider starting with hybrid funds or getting advice from a mutual fund consultant)

Conclusion

The equity vs debt mutual fund choice is not about which is universally better — it is about which is better for you, at this stage of your financial life.

Equity funds are the engine of long-term wealth creation. With historical returns of 9%–12% CAGR and the power of compounding, they are the most effective tool to build substantial wealth over 5–10 years and beyond. Debt funds, on the other hand, are the stabiliser — preserving capital, delivering predictable returns, and serving shorter time horizons effectively.

The smartest approach for most investors is a mix of both, calibrated to their goals, risk tolerance, and timeline. As you move closer to your financial goals, gradually shifting from equity to debt reduces risk and protects the wealth you have built.

Whether you are just starting your investment journey or looking to optimise an existing portfolio, a qualified mutual fund advisor or mutual fund consultant from Fincart can provide the personalised guidance you need to make the right call — every step of the way.

Frequently Asked Questions (FAQs)

1. Which is better — equity or debt mutual fund?

Neither is universally better. Equity mutual funds are better for long-term wealth creation (5+ year horizon) with higher returns but higher risk. Debt mutual funds are better for short-term goals (1–3 years) with lower but stable returns. The right choice depends on your financial goals, risk tolerance, and investment horizon. A mutual fund advisor can help you decide.

2. What is the main debt and equity mutual funds difference?

The core debt and equity mutual funds difference lies in where the money is invested. Equity funds invest in company stocks for capital appreciation. Debt funds invest in fixed-income instruments like bonds and treasury bills for stable income. They differ significantly in risk level, return potential, taxation, and suitability.

3. What are the tax rules for equity vs debt mutual fund in 2026?

For equity funds: STCG is taxed at 20% (held < 12 months); LTCG above ₹1.25 lakh is taxed at 12.5% (held > 12 months). For debt funds: STCG is taxed at your income slab rate (held < 24 months); LTCG is taxed at 12.5% without indexation (held > 24 months).

4. Can I invest in both equity and debt mutual funds at the same time?

Yes — and in fact, most financial advisors recommend holding a mix of both. Equity provides growth; debt provides stability and liquidity. Balanced advantage funds and hybrid funds offer a single-fund solution that automatically manages this allocation.

5. What return can I expect from equity vs debt mutual fund?

Equity mutual funds have historically delivered 9%–12% CAGR over 5–10 year periods. Debt mutual funds typically return 6%–8% per year depending on the fund type and interest rate environment. Returns are never guaranteed and vary based on market conditions.

6. How do I choose the right mutual fund for my goals?

Start with your goal, timeline, and risk appetite. Short-term goals with low risk tolerance → debt funds. Long-term goals with higher risk tolerance → equity funds. When in doubt, speak to a mutual fund consultant who can map the right funds to your specific needs.

7. Is a debt mutual fund safer than a fixed deposit?

Debt mutual funds are generally considered low risk but are not as safe as bank fixed deposits (which are insured up to ₹5 lakh by DICGC). However, debt funds may offer better post-tax returns in some cases. The right choice depends on your liquidity needs and tax bracket.

Disclaimer: Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. Past performance is not indicative of future results. The information in this article is for educational purposes only and does not constitute investment advice. Please consult a registered mutual fund advisor or mutual fund consultant before making investment decisions.