Income Tax Slabs and Rates for 2026 (AY 2026-27)

Filing your income tax return starts with one basic question: which slab does your income fall into? The income tax slab 2026 structure decides how much tax you owe, and getting this wrong can mean overpaying or facing a notice later. This article breaks down the income tax slab 2026 rates for Assessment Year 2026-27, corresponding to Financial Year 2025-26, so you know exactly where you stand before you file.

Understanding Financial Year and Assessment Year

Before looking at the numbers, it helps to clear up one common confusion:

Financial Year (FY) is the year in which you actually earn your income. For this guide, that is FY 2025-26, running from April 1, 2025, to March 31, 2026.

Assessment Year (AY) is the year in which that income gets assessed and taxed. For income earned in FY 2025-26, the assessment year is AY 2026-27.

The Income Tax Act, 2025, comes into effect from April 1, 2026, but for income earned up to March 31, 2026, the older 1961 Act provisions still apply.

India offers taxpayers a choice between two systems. The new tax regime, under Section 115BAC, is the default option and offers lower rates but removes most deductions. The old tax regime allows you to claim deductions like Section 80C, 80D, HRA, and home loan interest, but at comparatively higher rates. You can choose either regime while filing your return, and salaried individuals can switch between the two every year.

Income Tax Slab 2026: New Tax Regime Rates

The new regime is the default choice for taxpayers filing under the income tax slab 2026 framework. Here are the applicable slabs for FY 2025-26 (AY 2026-27):

Income Range | Tax Rate |

Up to Rs. 4,00,000 | Nil |

Rs. 4,00,001 to Rs. 8,00,000 | 5% |

Rs. 8,00,001 to Rs. 12,00,000 | 10% |

Rs. 12,00,001 to Rs. 16,00,000 | 15% |

Rs. 16,00,001 to Rs. 20,00,000 | 20% |

Rs. 20,00,001 to Rs. 24,00,000 | 25% |

Above Rs. 24,00,000 | 30% |

The Rs. 12 lakh tax-free benefit: One of the biggest highlights of the income tax slab 2026 under new tax regime structure is the enhanced rebate under Section 87A. If your net taxable income is up to Rs. 12,00,000, you get a full rebate of up to Rs. 60,000, bringing your tax liability to zero. Salaried employees also get a standard deduction of Rs. 75,000, so gross salary up to roughly Rs. 12,75,000 can remain completely tax-free. This rebate does not apply to income taxed at special rates, such as capital gains from shares or property.

Income Tax Slab 2026: Old Tax Regime Rates

If you prefer to claim deductions, you can opt for the old regime. The slabs depend on your age category:

Below 60 years:

Income Range | Tax Rate |

Up to Rs. 2,50,000 | Nil |

Rs. 2,50,001 to Rs. 5,00,000 | 5% |

Rs. 5,00,001 to Rs. 10,00,000 | 20% |

Above Rs. 10,00,000 | 30% |

Senior citizens (60 to 79 years):

Income Range | Tax Rate |

Up to Rs. 3,00,000 | Nil |

Rs. 3,00,001 to Rs. 5,00,000 | 5% |

Rs. 5,00,001 to Rs. 10,00,000 | 20% |

Above Rs. 10,00,000 | 30% |

Super senior citizens (80 years and above):

Income Range | Tax Rate |

Up to Rs. 5,00,000 | Nil |

Rs. 5,00,001 to Rs. 10,00,000 | 20% |

Above Rs. 10,00,000 | 30% |

Under the old regime, the Section 87A rebate applies only if taxable income does not exceed Rs. 5,00,000, with a maximum rebate of Rs. 12,500.

Surcharge and Cess

Apart from the basic income tax slab 2026 rates, two more components affect your final bill:

Health and Education Cess: Every taxpayer pays a flat 4% cess on the total tax amount (including surcharge, if any), regardless of income level, and this stays the same across both regimes.

Surcharge: This applies only above certain high income thresholds. Under the new regime, surcharge is capped at 25% for income above Rs. 2 crore. Under the old regime, it can go up to 37% for income above Rs. 5 crore. If your income falls just above these thresholds, you can claim marginal relief so you don't end up paying disproportionately more tax for a small increase in income.

Tax Saving Under New Tax Regime: Slab-Wise Comparison

The income tax slab 2026 rates are structured to make the new regime attractive across almost every bracket. Here's an approximate comparison of tax liability (before cess, assuming no deductions claimed):

Taxable Income | Old Regime | New Regime | Approx. Savings |

Rs. 5,00,000 | Nil | Nil | No difference |

Rs. 8,00,000 | Rs. 72,500 | Nil | Rs. 72,500 |

Rs. 10,00,000 | Rs. 1,12,500 | Nil | Rs. 1,12,500 |

Rs. 12,00,000 | Rs. 1,72,500 | Nil | Rs. 1,72,500 |

Rs. 15,00,000 | Rs. 2,62,500 | Rs. 1,05,000 | Rs. 1,57,500 |

Rs. 20,00,000 | Rs. 4,12,500 | Rs. 2,00,000 | Rs. 2,12,500 |

Rs. 25,00,000 | Rs. 5,62,500 | Rs. 2,50,000 | Rs. 3,12,500 |

Income up to Rs. 12 lakh benefits the most, since the Section 87A rebate wipes out tax entirely under the new regime. Middle-income earners between Rs. 12 lakh and Rs. 20 lakh see steadily growing savings, thanks to the wider 4-lakh slab bands. Higher earners above Rs. 20 lakh continue to save, though the gap narrows slightly since the top 30% rate kicks in earlier under the old regime.

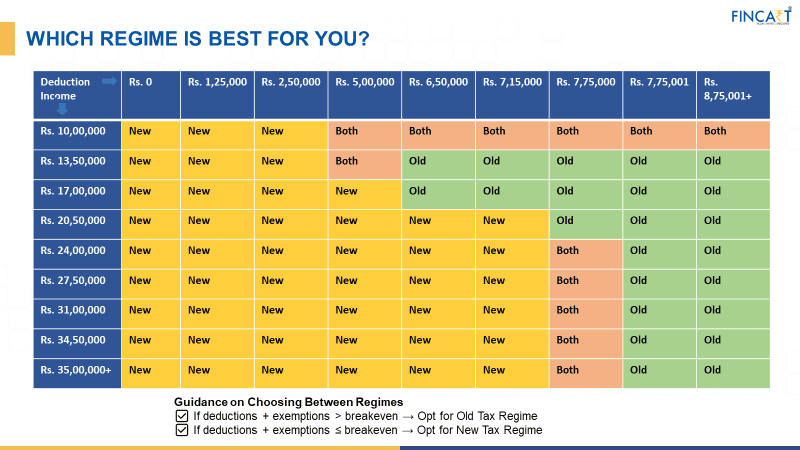

This table assumes no deductions under the old regime. If you have a large home loan interest claim or fully utilise Section 80C and 80D limits, the old regime can narrow or even reverse this gap. This is exactly the kind of calculation where a tax consultant makes a real difference, since the right answer depends on your specific deduction profile rather than general averages. Salaried individuals with simple income can usually rely on the new regime, while those with home loans, HRA, or heavy investments should compare both before deciding, ideally with help from tax consulting services rather than a rough estimate.

Income Tax Changes Effective From 1st April 2026

While the income tax slab 2026 rates themselves have not changed, April 1, 2026, still marks an important administrative shift:

Income Tax Act, 2025 replaces the 1961 Act – Section numbers have changed, so references like "Section 80C" or "Section 87A" now correspond to different section numbers, even though the underlying benefits remain the same.

New ITR forms – Updated forms are being rolled out to align with the new Act, meaning a short adjustment period while filing for the first time.

Extended revised-return window – Revised returns can now be filed up to March 31 of the relevant assessment year instead of the earlier December 31 cutoff, though a late fee applies.

Relief for NRI property transactions – TAN is no longer mandatory for TDS on property purchases involving NRI sellers; a PAN-based challan is used instead.

Simplified Form 15G/15H submission – These can now be submitted directly with depositories to reduce TDS on dividend and interest income, useful for retirees and fixed-deposit holders.

Higher deduction limit for senior citizens – The deduction threshold on interest income has been doubled, giving retirees a larger tax-free cushion.

No change to slabs, cess, or surcharge – The income tax slab 2026 rates, 4% cess, Section 87A rebate, and surcharge all remain unchanged from FY 2025-26.

None of these changes affect how much tax you owe. They affect how you file and how much paperwork certain transactions require. Since the new Act renumbers familiar sections, this is a good year to have a tax consultant review your filing even if your income hasn't changed much.

Key Deadlines and Common Mistakes

The due date to file your ITR for FY 2025-26 (AY 2026-27) is July 31, 2026, for individuals not requiring an audit. Missing it attracts late fees and interest on unpaid tax.

A few mistakes to watch for:

Assuming the new regime is automatically better without checking your actual deductions under the old regime.

Forgetting to claim the Rs. 75,000 standard deduction if you're salaried.

Missing the Section 87A rebate check, especially near the Rs. 12 lakh threshold.

Ignoring surcharge and cess while estimating total liability.

Overlooking capital gains, which are taxed at special rates and don't benefit from the Section 87A rebate.

Conclusion

The income tax slab 2026 structure continues to favor the new regime for most taxpayers, particularly with the Rs. 12 lakh tax-free threshold under Section 87A. But tax planning is rarely one-size-fits-all. Your income sources, deduction eligibility, and financial goals all play a role in deciding which regime works best.

If your situation involves multiple income streams, investments, or property transactions, it makes sense to consult a tax consultant rather than relying on generic calculators. Professional tax consulting services can help you factor in nuances like marginal relief, capital gains treatment, and regime-switching rules that are easy to miss when filing on your own. Getting this right early saves both money and stress when the deadline approaches.

Frequently Asked Questions (FAQs)

1. What is the income tax slab for 2026?

For FY 2025-26 (AY 2026-27), the income tax slab 2026 under the new regime is nil up to Rs. 4 lakh, then 5%, 10%, 15%, 20%, 25%, rising to 30% above Rs. 24 lakh. Income up to Rs. 12 lakh is effectively tax-free due to the Section 87A rebate.

2. Is income up to Rs. 12 lakh tax-free in 2026?

Yes. Under the income tax slab 2026 rules, resident individuals with taxable income up to Rs. 12 lakh pay zero tax under the new regime. This is due to a Section 87A rebate of up to Rs. 60,000, which cancels out the tax owed.

3. Old regime or new regime which is better in 2026?

It depends on your deductions. The income tax slab 2026 favors the new regime if you claim a few deductions. If you have large home loan interest, 80C investments, or HRA claims, the old regime may still save you more tax.

4. Did the income tax slabs change for 2026?

No. Budget 2026 made no changes to the income tax slab 2026 rates, surcharge, or cess. The slabs introduced in Budget 2025 continue unchanged for both FY 2025-26 and FY 2026-27 under the new regime.

5. What is the last date to file ITR for AY 2026-27?

The due date to file returns under the income tax slab 2026 rules is July 31, 2026, for individuals not requiring an audit. Filing after this date attracts late fees and interest on any unpaid tax.

Disclaimer: This article is intended for informational purposes only and does not constitute tax advice. Tax laws and deadlines are subject to change. Please consult a qualified tax consultant before making any filing decisions.

Read Important Disclosures

You Might Also Like

Do It Yourself. Do It Smarter.

Download DIY App available on App Store & Google Play

OR